The $400 Billion Giant: Google’s AI Counteroffensive Explodes as Gemini Hits 750M Users

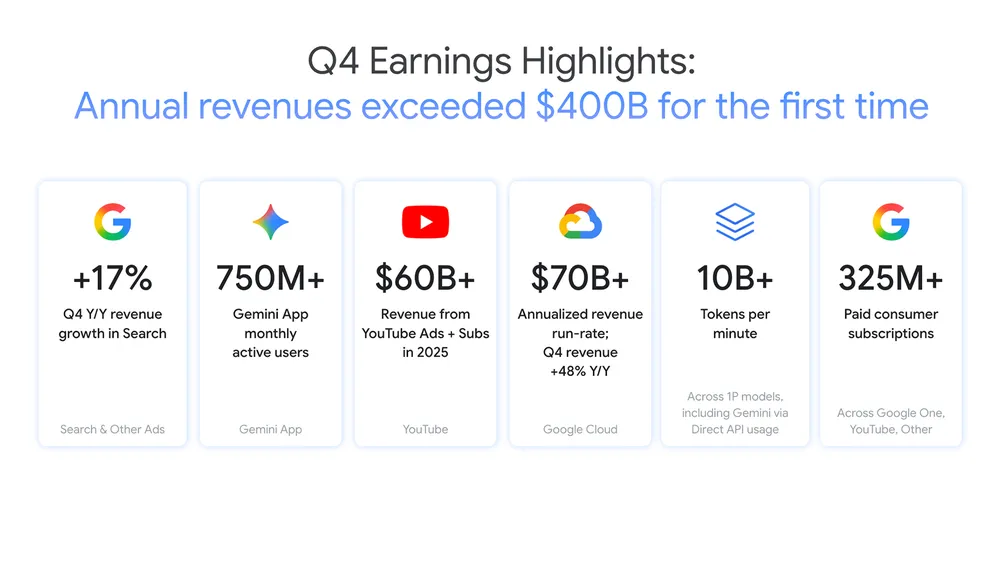

Propelled by the robust expansion of its Cloud services and YouTube, Alphabet’s annual revenue has, for the first time, eclipsed the $400 billion threshold, marking a 15% year-over-year increase. Beyond this fiscal milestone, Google CEO Sundar Pichai disclosed during the earnings call that the monthly active users (MAU) of the Gemini App have officially surged past 750 million. This suggests that following the inauguration of the Gemini 3 model, Google’s strategic counteroffensive in the artificial intelligence arena is yielding significant results.

According to fiscal telemetry, the Gemini App’s MAU escalated from 650 million in the preceding quarter to 750 million within a single term—a rapid ascent attributed to the launch of Gemini 3 last November. Pichai characterized Gemini 3 as the most rapidly adopted model in the corporation’s history. In contrast, Meta AI currently commands approximately 500 million MAUs, while ChatGPT’s late-2025 projections hover between 810 million and 900 million, indicating that the chasm between Google and OpenAI is narrowing with remarkable velocity.

Furthermore, Google’s API utilization is staggering, processing in excess of 10 billion tokens per minute. Pichai also alluded to a profound collaboration with Apple, wherein a bespoke iteration of Gemini 3 will empower the new Siri digital assistant, a partnership poised to catalyze further surges in usage.

Beyond the AI frontier, traditional sectors continue to flourish as primary revenue drivers:

-

YouTube: Combined annual revenue from advertising and subscriptions has surpassed $600 billion, with Nielsen data confirming its continued hegemony in the streaming market.

-

Google Cloud: The annual revenue run rate has reached a formidable $70 billion.

-

Subscription Services: Paid subscribers for Google One and YouTube Premium collectively exceed 325 million.

To sustain these colossal computational exigencies, Alphabet anticipates its capital expenditure for 2026 to fall between $175 billion and $185 billion—nearly doubling its 2025 investments. This immense capital is earmarked for the expansion of silicon procurement—including proprietary Ironwood TPUs and NVIDIA GPUs—alongside the continued development of data center infrastructure. Despite these stellar financial results, such aggressive expenditure induced marginal market trepidation, resulting in a 2% decline in Alphabet’s share price post-announcement.

From an analytical perspective, Google’s AI strategy has transitioned from defensive preservation to a potent offensive posture, demonstrating clear monetization capabilities. While the market previously feared that AI would cannibalize search advertising revenue, Google has stabilized its position through a “hybrid monetization” model encompassing enterprise cloud services, consumer subscriptions, and search ads. The triumph of Gemini 3 underscores Google’s profound algorithmic heritage.

As the AI arms race evolves into a contest of fiscal depth and computational abundance, Google’s reliance on its in-house TPU architecture may afford it a strategic advantage in cost containment over rivals exclusively dependent on external silicon. The next focal point of observation remains the maturation of “Agentic AI.” Google has teased the integration of “transactional capabilities” within Gemini, signifying a shift from mere conversational interfaces to autonomous assistants capable of executing complex tasks—the definitive “Holy Grail” of AI commercialization.

Related Posts:

Support Our Threat Intelligence

If you find our CVE report and cybersecurity news helpful, consider supporting our work.